The governance gap continues to widen as financial workflows become more automated with AI.

Other AI tools lack transparency that cannot be reliably audited or explained to stakeholders.

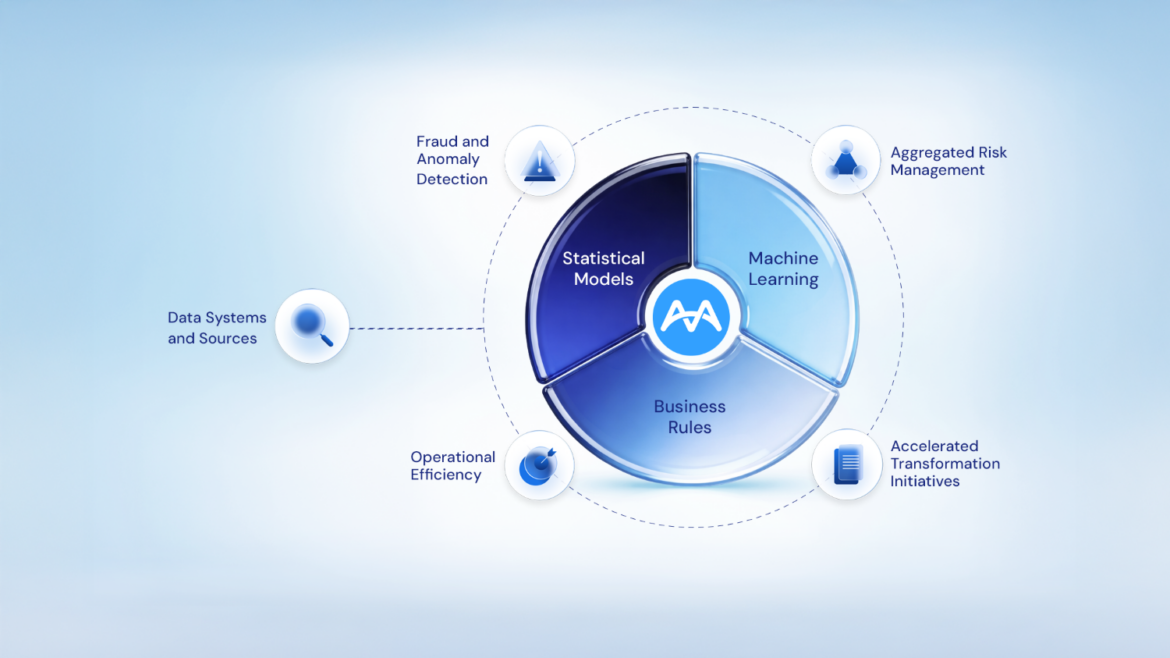

Narrow the gap with an independent oversight layer above and across all financial systems of record.

Reduce financial risk, improve efficiency, and deliver greater confidence in your numbers with full explainability.