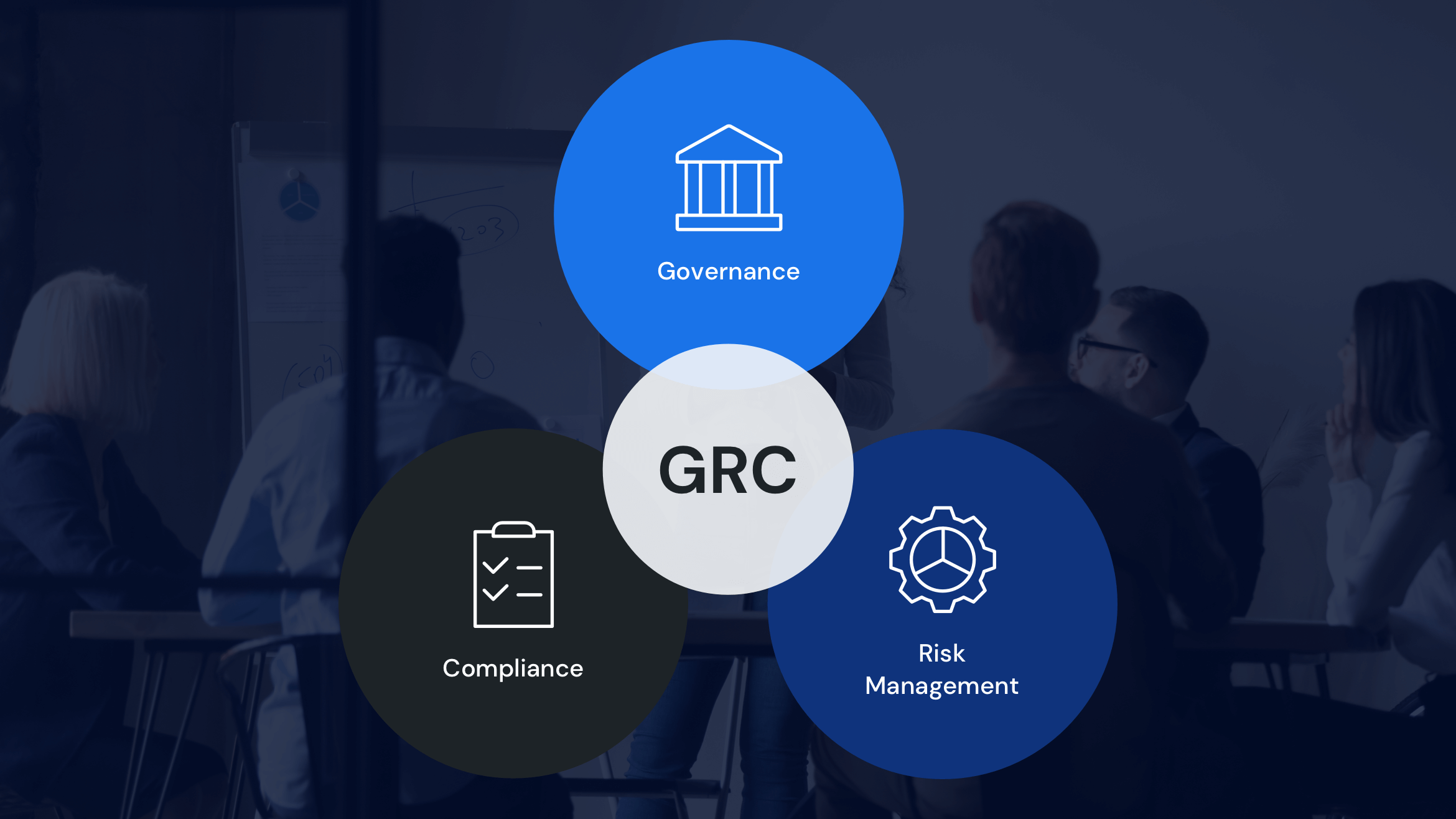

Why Financial Risk Oversight Must Evolve in an Era of Constant Change

Guest Contributor Michael Rasmussen CEO, GRC 20/20 Research Editor’s Note: This guest article by Michael Rasmussen expands on themes discussed during MindBridge’s webinar, Building Resilient Financial Risk Oversight in an Era of Constant Change. The Pace of Financial Risk Has Changed Financial risk does not wait patiently for the end of the month, the completion of the … Read more